Americas Oil Supply Routes

Status of the critical maritime chokepoints and infrastructure affecting Western Hemisphere fuel supply. The transit, port-flow and sea-state panels below refresh daily from satellite-AIS and weather feeds; the chokepoint risk assessments further down are maintained editorially.

→ Strait of Hormuz crisis timeline — a sourced, filterable chronology of the 2026 crisis.

Global Supply Chokepoints — Risk Overview

Chokepoint Transit Monitor

Tanker tonnage (DWT) vs 2023 baseline · IMF PortWatch (AIS estimates)Strait of Hormuz tanker tonnage is at 9% of normal, with Suez Canal and Bab el-Mandeb Strait also restricted; traffic is rerouting via the Cape of Good Hope (178% of baseline).

Crude- and product-carrying capacity actually moving through each chokepoint — weighted by tanker size (a VLCC isn’t a coastal product tanker).

Latest data 2026-06-21 (≈9 days ago) — PortWatch reports in arrears, so it confirms shifts after the fact, not in real time. The % is tanker capacity (DWT) vs the 2023 daily average (trailing 7-day); ship counts shown for context. Lanes marked AIS low are conflict zones where spoofing, jamming or vessels going dark can make figures undercount actual movement. Source: IMF PortWatch — estimated from satellite AIS, not customs data. PortWatch does not tell us the exact barrel, grade or buyer — only whether the ships needed to move the oil economy are actually moving.

Panama Canal Watch

Live transit vs 2023 · IMF PortWatch (AIS estimates)The Western Hemisphere’s key chokepoint — the Pacific↔Atlantic shortcut that keeps US Gulf and East Coast cargoes off the long route around South America.

Watch the draft, not just the count: Panama’s throughput is rationed by Gatún Lake water levels, and drought has forced deep transit cuts before (2023–24). A dry season that lowers the lake squeezes daily slots and pushes more tonnage onto the longer Cape Horn / Suez routes. Latest data 2026-06-21 (PortWatch reports ~a week in arrears). Source: IMF PortWatch — transit estimated from satellite AIS, not canal-authority counts.

Port Oil-Flow Monitor

Tanker import/export vs 2023 baseline · IMF PortWatch (AIS estimates)Crude and product moving through major hubs — daily tanker tonnage in (↓) and out (↑), with how it compares to the 2023 average. Where the barrels are actually going.

Americas

Global oil hubs

Latest data 2026-06-19 (PortWatch reports ~a week in arrears — it confirms shifts after the fact, not in real time). Volumes in thousand tonnes/day (kt/d), trailing 7-day average vs 2023. Source: IMF PortWatch — tanker tonnage estimated from satellite AIS, not customs data; some terminals (e.g. Gulf export ports) are under-covered and read low.

Live Sea State — Oil Shipping Chokepoints

Significant wave height, wave period, and 10-metre wind speed. Updated 29 Jun, 10:58 UTC.

Strait of Hormuz

Persian Gulf / Gulf of Oman

0.66m

wave height

3.4s

period

12kt · g15SW

wind

Bab el-Mandeb

Red Sea / Gulf of Aden

0.76m

wave height

3.3s

period

19kt · g31NNW

wind

Panama Canal (Caribbean approach)

Caribbean

1.50m

wave height

7.3s

period

8kt · g16N

wind

Strait of Florida

Gulf of Mexico / Atlantic

0.76m

wave height

4.5s

period

11kt · g12E

wind

Source: Open-Meteo Marine + Forecast APIs (sourced from European met agencies). Risk band uses Douglas-style sea-state (wave height) and Beaufort-style wind thresholds; whichever is worse sets the band. open-meteo.com ↗

Current Route Status

Risk levels: Normal · Elevated · High · Critical

US Maritime Security Advisories

MARAD active advisories relevant to Americas supply routes · Updated Jun 29, 2026

Global

U.S. Maritime Advisory Updates, Resources, and Contacts

Red Sea, Bab el Mandeb Strait, Gulf of Aden, Arabian Sea, and Somali Basin

Houthi Attacks on Commercial Vessels

Persian Gulf, Strait of Hormuz, and Gulf of Oman

Iranian Attacks on Commercial Vessels

Gulf of Aden, Arabian Sea, Indian Ocean

Piracy/Armed Robbery/Kidnapping for Ransom

Red Sea, Bab el Mandeb Strait, Gulf of Aden, Arabian Sea, Persian Gulf, and Somali Basin

Houthi Attacks on Commercial Vessels

Gulf of Aden, Arabian Sea, Indian Ocean

Piracy/Armed Robbery/Kidnapping for Ransom

Strait of Hormuz and Gulf of Oman

Iranian Illegal Boarding / Detention / Seizure

Global

U.S. Maritime Advisory Updates, Resources, and Contacts

Gulf of Aden, Arabian Sea, Indian Ocean

Piracy/Armed Robbery/Kidnapping for Ransom

Source: US Maritime Administration (MARAD). Full advisory text on MARAD site.

Thermal Anomalies — Major Refineries & Terminals

NASA FIRMS VIIRS satellite detections within ~15 km of major US Gulf, US East/West Coast, Caribbean and Latin American refineries. Past 24 h. High Fire Radiative Power near a facility may indicate flaring, fire, or process incident — not all detections indicate incidents.

Energy Research — CREA

Russian fossil fuel exports, Hormuz impacts & Americas supply analysis · Updated Jun 29, 2026

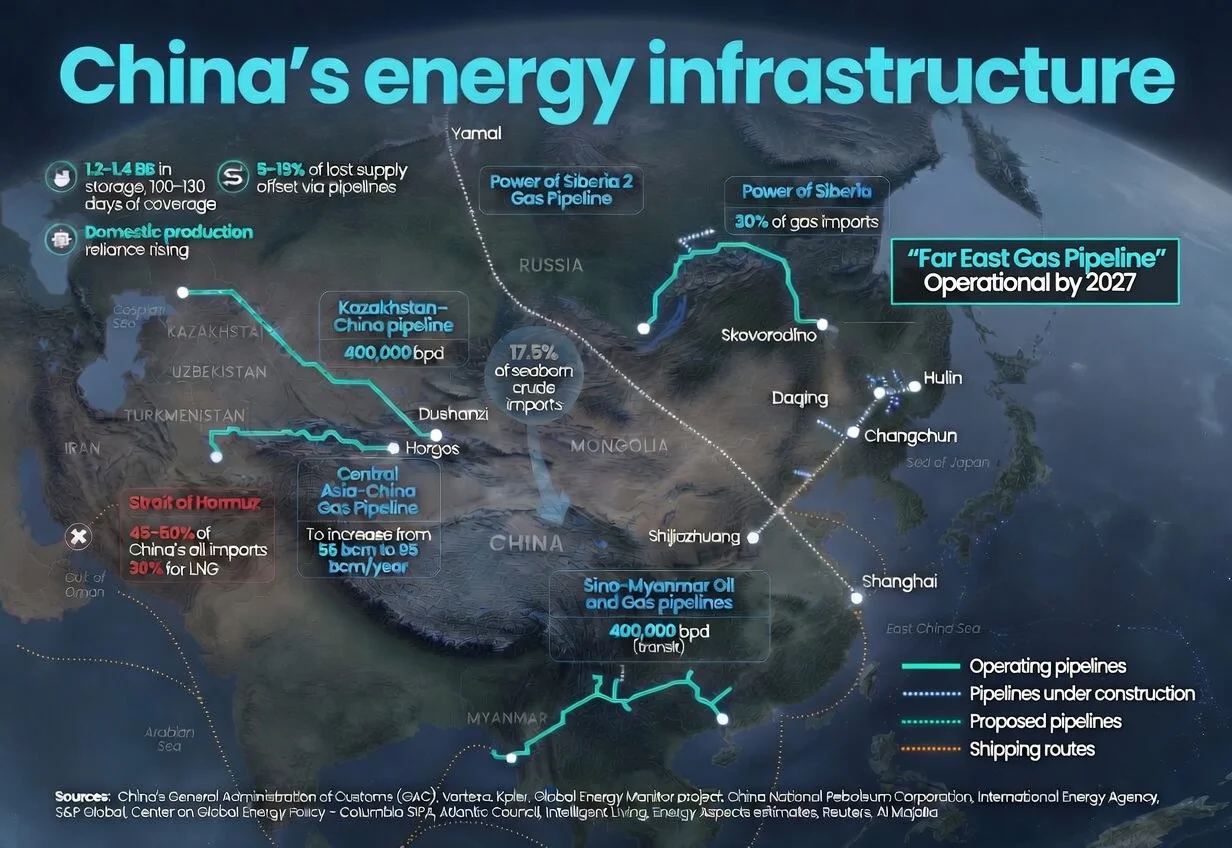

China Energy and Emissions Trends – May 2026 snapshot

Indonesia’s currency crisis: Fossil fuel dependence and subsidies a key driver

May 2026 — Monthly analysis of Russian fossil fuel exports and sanctions

Analysis: China’s new carbon metric leaves Germany-sized gap in its emissions

What drove China’s historic drop in power-sector emissions?

China Energy and Emissions Trends – April 2026 snapshot

April 2026 — Monthly analysis of Russian fossil fuel exports and sanctions

Quarterly energy snapshot for India: Q4 2025-26

Active Disruption Risk

Strait of Hormuz

Persian Gulf / Gulf of Oman · 26.5°N 56.4°E

Critical — tanker tonnage at 9% of the 2023 norm (live · IMF PortWatch)

The Strait of Hormuz remains the master variable for global oil. After the conflict that began in late February 2026 effectively closed it, the EIA assumed Hormuz stayed shut into late May, with traffic only beginning to pick up in June. Iran now says it will reopen only under new conditions — including possible Oman-set transit fees, which Washington opposes. All major Gulf producers export through this single chokepoint; in practice only a handful of crude, product and LNG vessels have exited recently — often with AIS gaps or under heightened risk — while overall Gulf flows stay far below normal. Open on paper, restricted in practice.

Americas Impact

US Gulf and East Coast refineries that process Gulf sour crude face spot-market tightness. The WTI-Brent spread has moved as Gulf crude stays hard to source globally, and Atlantic-basin producers (US shale, Brazil, Guyana) are the substitution pool. Saudi Arabia cut July official selling prices to Asia by $6/bbl, signalling demand destruction. SPR drawdown contingencies remain in play.

Context

Hormuz is Washington's top priority and Tehran's main leverage in unresolved US–Iran talks. The early-June Israeli strike on Iran's Mahshahr petrochemical complex — the first hit on Iranian energy infrastructure since the April ceasefire — put a direct energy-asset risk premium back on. Even after a reopening, recovery is slow: Kuwait says it could restore ~70% of output within 6–8 weeks, the rest taking roughly another month.

Last reviewed: 2026-06-21

Bab-el-Mandeb Strait

Red Sea / Gulf of Aden · 12.6°N 43.3°E

Critical — MARAD 2026-006: Houthi Attacks on Commercial Vessels

Houthi forces in Yemen have attacked over 100 commercial vessels since November 2023, effectively closing the Red Sea route to most shipping. Combined with the still-constrained Hormuz corridor, both primary Gulf export corridors remain under simultaneous pressure — an unprecedented compound event, with renewed Houthi threats an active watch-item.

Americas Impact

The Cape of Good Hope reroute adds 10-14 days each way and increases shipping costs significantly. For Americas-bound Gulf crude, this compounds with the constrained Hormuz corridor to force spot-market substitution from Atlantic Basin producers (US shale, Brazil, Guyana).

Context

US and allied naval operations (Operation Prosperity Guardian) have not deterred attacks. Most major shipping lines continue to avoid the route. Insurance premiums for Red Sea transits remain at crisis levels.

Last reviewed: 2026-06-29

Normal Conditions

Panama Canal

Central America · 9.1°N 79.4°W

Normal — tanker tonnage near the 2023 norm (104%) (live · IMF PortWatch)

The Panama Canal handles roughly 5% of global seaborne trade and is the only non-Cape route between the Atlantic and Pacific in the Americas. Severe drought in 2023-2024 forced vessel restrictions to 24/day (down from 36), causing major disruption and wait times of 10+ days. Wet-season levels have since restored near-normal transits; the risk window is the dry season (~Dec–Apr), when low Gatún Lake levels can again force draft and slot cuts.

Americas Impact

Drought-linked restrictions in 2023-24 added $300-500M in annual shipping costs. US LNG exporters diverted cargoes around Cape Horn. Alaska crude exports to Gulf Coast refineries delayed. El Niño patterns drive multi-year drought cycles.

Context

Canal expansion completed 2016 allows Neo-Panamax vessels up to 14,000 TEU. However, Gatun Lake water levels remain the binding constraint. Climate change projections suggest increasing drought frequency. Alternative: Cape Horn route adds ~8,000 nautical miles.

Last reviewed: 2026-06-21

Straits of Florida

Caribbean / Southeast US · 24.5°N 80.2°W

Normal — open, routine monitoring

The Straits of Florida (between Cuba and the Florida Keys) carry significant volumes of refined petroleum products northward to US East Coast markets, and crude southward. Major US refineries in the Gulf Coast export through this route.

Americas Impact

No current disruption risk. The strait is under US Coast Guard jurisdiction and routinely monitored. Any disruption would force rerouting around Cuba, adding 2-3 days transit.

Context

US-Cuba relations and Cuban political stability are the primary geopolitical risk factors. Cuba's deteriorating economy and fuel shortages occasionally affect shipping logistics.

Last reviewed: 2026-04-19

Gulf of Mexico

Southern US / Mexico · 25°N 90°W

Normal — hurricane season monitoring begins June

The Gulf of Mexico is both a major producing basin and the hub of US petroleum logistics. Eight of the top US refineries by capacity are on the Gulf Coast. Hurricane season (June-November) is the primary annual risk — major storms like Katrina (2005) and Ida (2021) caused significant and lasting supply disruptions.

Americas Impact

A major hurricane strike on the Houston Ship Channel or Port Arthur refining complex would be a national supply emergency. US EIA monitors GoM production weekly. The 2024 hurricane season was above average but major refineries were spared.

Context

Offshore platforms are increasingly hurricane-hardened, but evacuation protocols still shut production for days to weeks per major storm. Pipeline infrastructure is the most vulnerable single-point-of-failure.

Last reviewed: 2026-04-19

Strait of Magellan

Southern Chile / Argentina · 54°S 70°W

Normal — alternative Cape route open

The Strait of Magellan and Drake Passage (around Cape Horn) provide the only alternatives to the Panama Canal for Pacific-Atlantic transit in the Western Hemisphere. The Magellan Strait is restricted to vessels under 280m length and 11.5m draught.

Americas Impact

During 2023-24 Panama Canal drought restrictions, some vessels rerouted via Cape Horn, adding ~8,000 nautical miles. Not economically viable for routine trade but important as overflow capacity.

Context

Extreme weather in the Drake Passage makes it dangerous for smaller vessels. The Magellan Strait requires pilot compulsion for commercial vessels. Argentina and Chile maintain the route.

Last reviewed: 2026-04-19