Why a Hormuz Shutdown Doesn't Automatically Mean $200 Oil

There's a tidy piece of logic floating around energy commentary: the Strait of Hormuz carries about a fifth of the world's oil, so if it closes, prices rocket to $200 and stay there. It feels obvious. It's also wrong — or at least far too simple. A sustained closure breaks that intuition in both directions, and understanding why is more useful than fixating on a single scary number.

The arithmetic nobody finishes

Hormuz moves roughly 20 million barrels a day — close to 20% of global liquids. Here's the part the $200 headlines skip: if that volume is genuinely gone for the foreseeable future, $200 isn't the nightmare number. It's almost optimistic.

The world's strategic chokepoints. For Gulf crude, Hormuz is the front door — and the only sea-route alternative is the weeks-longer haul around the Cape of Good Hope.

You cannot price your way out of losing 17–20 million barrels a day from a ~103 million barrel market. Price doesn't clear a gap that size — physical rationing does. Fuel queues, allocation, export bans. So the "it goes to $200" framing actually understates the short-term chaos of a true cutoff.

But the same fact that makes the spike violent is what stops it from sitting there.

Three brakes on a permanent $200

Bypass capacity exists — just not enough. Saudi Arabia's East–West (Petroline) pipeline to the Red Sea and the UAE's Habshan–Fujairah line can route maybe 3.5 million barrels a day around the strait. That blunts the worst case. It replaces a fraction, not the whole.

Strategic reserves buy time, not supply. Coordinated releases from the US, IEA members, and China can cover a gap for months. Then they're empty — and after the heavy 2022 drawdowns, the US reserve in particular starts this crisis well below its historic fill. Reserves flatten the spike; they don't refill the pipeline.

Demand destruction is fast and brutal at these prices. $200 oil triggers recession. Recession destroys demand. Falling demand drags price back down — not to anything comfortable, but off the peak. High prices are self-limiting; the catch is that the mechanism is the recession.

The realistic shape: a path, not a number

Put those together and the honest picture isn't "rises to $200 and holds." It's a sequence:

- Violent spike on the disruption — potentially overshooting $200 briefly as markets panic and inventories draw.

- Reserve drawdown caps the peak and buys a few months of breathing room.

- Demand destruction sets in as the economy contracts and the highest-value uses crowd out the rest.

- A new, lower-but-still-elevated equilibrium, with the floor set by how much bypass capacity, reserves, and rationing actually absorb.

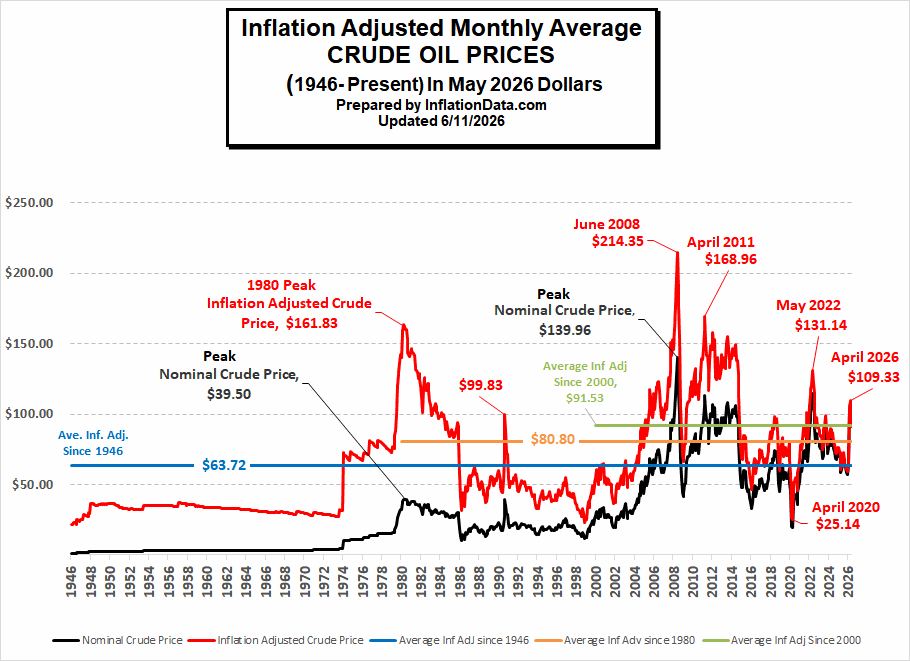

History has already run this experiment. In June 2008, crude touched roughly $214 a barrel in today's money — and then collapsed within months as the economy buckled. That's not a footnote; it's the entire pattern in one chart.

Inflation-adjusted crude, 1946–present. Every great spike — 1980, 2008, 2022 — is followed by a fall. The peak is never the equilibrium. Source: InflationData.com.

That path is a far more useful mental model than any single price tag.

The premise is the real weak point

The whole scenario hinges on one assumption: that the strait stays shut indefinitely. That's the part doing the heavy lifting — and it's the shakiest.

- Iran exports through Hormuz too. A total, indefinite closure strangles Iran's own oil revenue.

- China is Iran's biggest Gulf customer and its economic lifeline. Beijing absorbs more pain from a closure than almost anyone and has every incentive to lean on Tehran to keep it open.

This is why a sustained total closure is a low-probability event — not because it's militarily hard to harass the strait (it isn't), but because a permanent seal is close to mutual economic suicide, Iran included. The realistic threat is intermittent disruption plus a fat, permanent risk premium — oil structurally elevated and choppy — not a clean, lasting cutoff.

A note on "the West has no cards"

It's tempting to read the standoff as the US holding a losing hand. In aggregate that's overstated — America is the world's largest crude producer (~13 million barrels a day) and, on net, imports little Gulf oil. But "energy independent on paper" hides three real vulnerabilities worth naming:

- The SPR is already drawn down. The Strategic Petroleum Reserve was run down hard in 2022 and sits well below its historic highs. The "reserves buy time" card is real — but the US has been spending it, partly to cushion global prices, and a fresh crisis starts from a thinner buffer than the headlines imply.

- National numbers hide regional islands — PADD 5 above all. The West Coast is effectively cut off from the rest of the US pipeline network; no major lines cross the Rockies. California and its neighbours lean on declining local output, Alaskan crude, and waterborne imports, some of it foreign. The Gulf Coast may be comfortable, but the West Coast is genuinely exposed to seaborne supply and price — and already pays the highest pump prices in the country.

- Volume isn't the same as grade. US shale is light and sweet; much of the US refining fleet is built for heavier, sourer crude it still imports. Being a net exporter by barrels doesn't mean having the right barrels. A disruption that pulls medium and heavy Gulf grades off the market still squeezes US refiners' feedstock and the products they can make.

So "least exposed" holds only in aggregate, and only relative to China, Japan, South Korea, India, and Europe — who would be hit far harder. The US isn't insulated; it's better cushioned, and even that cushion is thinner than it used to be.

Iran's leverage, meanwhile, is real but asymmetric: it's the power to impose global costs cheaply, not the power to win a standoff — and using it hurts Iran and China most of all. That's leverage to inflict pain, not to dictate terms.

Bottom line

A genuinely indefinite Hormuz closure wouldn't inevitably deliver a stable $200. It would deliver a chaotic spike that could blow past $200 briefly, then drift down under the weight of demand destruction, settling at a floor determined by bypass routes, reserves, and rationing. And the scenario most likely to actually persist is recurring disruption and a structural risk premium — not a permanent cutoff — precisely because a permanent cutoff is the one thing no one, Iran included, can really afford.

Watch the path, not the number.